30-Year, Maybe 50-Year Mortgage, But Transferable Mortgage Is Best

In the evolving landscape of American housing finance, the conversation around mortgage terms has taken a dramatic turn. With home prices soaring and affordability challenges reaching crisis levels, President Donald Trump has proposed extending the standard 30-year mortgage to a staggering 50 years. Announced in early November 2025, this idea—championed by Federal Housing Finance Agency (FHFA) Director Bill Pulte as a "complete game changer"—aims to lower monthly payments and unlock homeownership for younger buyers priced out of the market.Backed by government-sponsored enterprises like Fannie Mae and Freddie Mac, the proposal could reshape lending norms, but it comes with significant trade-offs. As policymakers weigh this option against the entrenched 30-year model, an alternative emerges: the transferable, or "portable," mortgage. This underutilized tool could offer the flexibility modern homebuyers crave without the long-term pitfalls of ultra-extended terms. In this article, we break down the pros and cons of the 50-year mortgage, contrast it with the 30-year standard, and make the case for why portability might be the superior path forward—strictly for individual primary residence owners.

The 50-Year Mortgage Proposal: A Bold Bid for Affordability

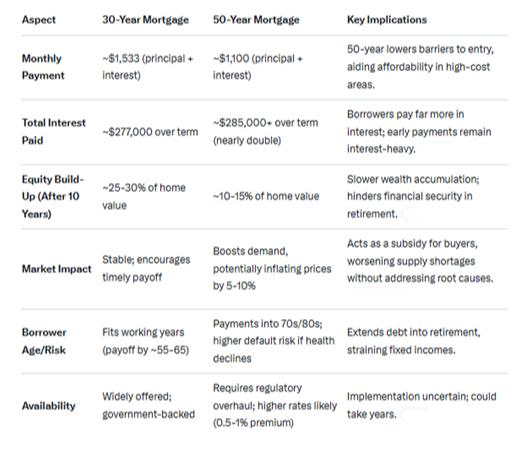

The roots of the 30-year mortgage trace back to the New Deal era of the 1930s, when it was designed as a sustainable product for families to pay off homes during their prime working years, aligned with an average U.S. lifespan of just 66. Fast-forward to 2025, and that model feels strained amid a 4.7 million-unit housing shortage, stagnant supply, and interest rates hovering around 5%. Enter the Trump administration's pitch for 50-year loans: by stretching repayments over nearly two additional decades, monthly payments could drop by 20-30% compared to a 30-year term, potentially qualifying more first-time buyers for loans they couldn't otherwise afford. Implementation would require navigating Dodd-Frank regulations, which currently cap qualified mortgages at 30 years (with limited exceptions up to 40), and possibly congressional action to amend financial laws.FHFA oversight of Fannie and Freddie could fast-track pilots, but experts caution that this isn't a silver bullet—it's more of a "band-aid" on deeper issues like zoning restrictions and construction delays.Still, proponents argue it's a vital tool in a broader arsenal to revive the "American Dream" for millennials and Gen Z, who face median home prices exceeding $400,000 in many markets.

Breaking Down the Good and the Bad: 50-Year vs. 30-Year Mortgages

While the allure of lower payments is undeniable, the 50-year mortgage introduces complexities that could exacerbate wealth gaps and market distortions. Below, we compare it to the 30-year standard using a hypothetical $300,000 loan at 5% interest with a 5% down payment (resulting in a $285,000 principal). These figures illustrate key financial dynamics, though actual rates and fees would vary.

The Pros of a 50-Year Mortgage

- Enhanced Accessibility: For young buyers or those in expensive urban markets, the reduced monthly outlay could mean the difference between renting indefinitely and building equity. As Pulte noted, it's a "weapon" to target affordability for the under-35 crowd.

- Flexibility in Tough Times: Lower payments provide breathing room during economic dips, reducing foreclosure risks in the short term.

- Innovation Signal: It signals government commitment to housing, potentially spurring complementary policies like tax credits or streamlined permitting.

The Cons: A Double-Edged Sword

- Exploding Interest Costs: Over 50 years, borrowers could pay 86% more in interest than on a 30-year loan, turning homeownership into a lifelong financial drag. Critics like those at the Consumer Federation of America call it a "distraction" that erodes wealth-building potential.

- Delayed Equity and Retirement Risks: Homeowners build equity glacially, leaving many with minimal ownership stake even after a decade. This could trap families in underwater loans if values stagnate or health issues arise later in life.

- Inflationary Pressure: By supercharging buyer demand without boosting supply, it risks bidding up prices further—negating affordability gains and fueling inequality.

- Systemic Vulnerabilities: Lenders face prolonged exposure to defaults, and the secondary market (via Fannie/Freddie) could see higher premiums, passing costs to all borrowers.

In essence, while the 50-year option might open doors today, it could lock many into suboptimal financial futures tomorrow. The 30-year remains the gold standard for balancing affordability with prudent debt management.

Why a Transferable Mortgage Might Be the Smarter Alternative

If extended terms like 50 years feel like overreach, consider the transferable (or portable) mortgage—a feature allowing borrowers to carry their existing loan terms, including the low interest rate, to a new primary residence upon sale. This isn't a new invention; it's already available through select lenders and government programs, but expanding it could address mobility without the drawbacks of ultra-long amortization

Imagine locking in a 3% rate during a low-interest window, only to face 6%+ rates five years later when job opportunities demand a move. A portable mortgage lets you transfer that favorable deal, avoiding refinancing fees (often 2-5% of the loan) and rate resets.For a family upsizing from a $300,000 starter home to a $450,000 family abode, this could save tens of thousands in interest while preserving equity gains from the original property.

The Superiority of Portability

- Rate Lock-In for Life Changes: In an era of remote work and career shifts, Americans move every 5-7 years on average. Portability shields against rate volatility, keeping housing costs predictable and encouraging timely upgrades without penalty.

- Equity Preservation and Wealth Acceleration: Unlike a 50-year loan's slow build-up, portability lets you carry forward paid-down principal, accelerating net worth as you ladder into larger homes.

- Lower Systemic Risk: It promotes market fluidity—sellers aren't deterred by rate fears, easing inventory shortages—without inflating demand artificially.

- Cost Efficiency: Monthly payments stay manageable, but the term doesn't balloon, ensuring payoff aligns with retirement planning.

Critically, this benefit should be reserved for individuals purchasing primary residences—no corporations snapping up rentals, no vacation-home speculators. Eligibility could tie to IRS definitions of a principal dwelling, with income caps or first-time buyer preferences to prioritize working families. Lenders might require the new home to be of comparable or greater value, preventing abuse, while government backing (via FHA or VA analogs) could standardize it nationwide.

Conclusion: Prioritizing Flexibility Over Extension

The buzz around 50-year mortgages highlights a genuine crisis: homeownership rates for under-35s have plummeted to 37%, the lowest in decades. Yet, as experts from Realtor.com to TD Securities warn, this fix risks more harm than good by prioritizing short-term access over long-term stability.A transferable mortgage, by contrast, empowers true mobility—letting families keep their low rates and equity intact as life unfolds—without extending debt into old age or distorting markets.

Policymakers should pivot here: Amend FHFA guidelines to mandate portability in government-backed loans for primary homes, and incentivize private lenders with tax breaks. This targeted approach would democratize housing without the 50-year gamble. After all, the best mortgage isn't the longest—it's the one that adapts to you. As the affordability debate rages on, let's build a system that moves with America's families, not against them.